Analysis of trends and determinants of the «Big 4» companies in the global audit market

DOI:

https://doi.org/10.15587/2706-5448.2023.286076Keywords:

«Big 4» companies, global audit market, global gross domestic product, total global revenue of companiesAbstract

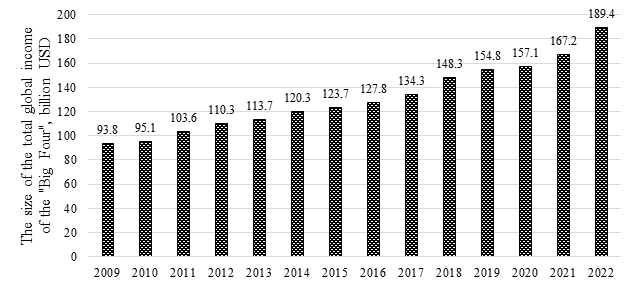

The object of research is the «Big 4» – a group of the largest international auditing companies, which includes: Deloitte (Great Britain), PricewaterhouseCoopers (USA), Ernst&Young (Great Britain) and KPMG (Netherlands). The target market of the «Big Four» companies is mainly large companies operating in various sectors of the world economy and regions of the world. Over the years, the «Big 4» companies have been leading the global audit services market and growing their revenues. Companies offer audit, tax and consulting services to their clients. This study is aimed at determining and evaluating the influence of the state of the world economy on the performance of companies and identifying the key endogenous determinants of the sustainability of their development. A comparative analysis of the dynamics of growth rates of global gross domestic product and aggregate global income of the «Big 4» companies during 2009–2022 showed their similarity, but not identity. The annual growth rates of the «Big 4» aggregate income mostly exceeded similar indicators of the global gross domestic product. The conducted correlation-regression analysis of the dependence of the aggregate revenues of the «Big 4» companies on the economic situation in the world confirmed the significant influence of the state of the world economy on the performance of the «Big 4» and made it possible to determine the level of this influence. A number of endogenous determinants contributing to the sustainable development of a group of companies in an unstable economic environment have been identified: the target segment (the largest international and national companies), broad industry diversification and geographical coverage of client companies, timely updating of the range of services in accordance with demand, effective international marketing strategies, use innovative technologies, highly professional management and company personnel.

References

- Auditing Services: Global Strategic Business Report. Research and Markets (2023). Global Industry Analysts, Inc, 163. Available at: https://www.researchandmarkets.com/reports/5140428/auditing-services-global-strategic-business

- Auditing Services Market Size And Forecast. Verified Market Research. Available at: https://www.verifiedmarketresearch.com/product/auditing-services-market/

- Rian, V. (2022). The Big Four Continue to Dominate Auditing: Weekly Stat. CFO. Available at: https://www.cfo.com/accounting-tax/auditing/2022/06/auditing-big-four-market-share-sec-registrants-accounting/

- Matthews, M. (2023). The Big 4 Accounting Firms: An Overview and Comparison. Available at: https://www.indeed.com/career-advice/career-development/big-4-accounting-firms

- PrepLounge. What Are the Differences Between the Big 4: KPMG, PwC, EY, Deloitte? (2023). Available at: https://www.preplounge.com/en/articles/differences-between-big-4

- Coello, K., Keohane, S. (2022). Who Audits Public Companies – United Kingdom 2021. Audit Analytics. Available at: https://blog.auditanalytics.com/who-audits-public-companies-united-kingdom-2021/

- The obstacles in the way of Big Four globalization (2021). Financial Times. Available at: https://www.ft.com/content/32c9277c-0bed-4d0e-aca1-0ef417a2bb15

- Petryk, O. A. (2010). Diialnist audytorskykh firm velykoi chetvirky: suchasni tendentsii rozvytku. Ekonomichni nauky. Seriia: Oblik i finansy, 7 (2), 481–491. Available at: http://nbuv.gov.ua/UJRN/ecnof_2010_7(2)__59

- Dvulit, Z., Melnyk, O., Lazurko, M. (2021). Research of the global market of audit services in the context of today’s challenges. Journal of Lviv Polytechnic National University. Series of Economics and Management Issues, 5 (2), 22–33. doi: https://doi.org/10.23939/semi2021.02.022

- Melnyk, N. H.; Tkachenko, S. A., Pashkevych, M. S. (Eds.) (2015). Osoblyvosti audytu na mizhnarodnomu rivni. Ekonomichna kryza: faktory, modeli ta mekhanizmy podolannia. Dnipropetrovsk: NHU, 143–152.

- Melnyk, M. V. (2018). Marketing Strategies in Contemporary Big Four Consulting Firms. Mechanism of an Economic Regulation, 4, 119–126. doi: https://doi.org/10.21272/mer.2018.82.11

- Khomenko, M. M. (2016). Suchasni tendentsii rozvytku audytorskoi diialnosti v Ukraini. Ekonomichnyi visnyk Dniprovskoi politekhniky, 3 (55), 113–119.

- Mulyk, Y. (2020). Audit activities in ukraine: current situation, reform and development. Agrosvit, 7, 37–47. doi: https://doi.org/10.32702/2306-6792.2020.7.37

- Top 10 Accounting Firms. (2023). Вig 4 accounting firms. Available at: https://big4accountingfirms.com/top-10-accounting-firms/

- Developments in Audit 2020 (2020). Financial Reporting Council. Available at: https://www.frc.org.uk/getattachment/58ac503e-a547-4f9e-8e52-16c7f5355586/Developments-in-Audit-2020.pdf

- Revenue of the Big Four accounting / audit firms worldwide in 2022, by function (in billion U. S. dollars) (2023). Statista Research Department. Available at: https://www.statista.com/statistics/250935/big-four-accounting-firms-breakdown-of-revenues/

- Combined revenue of the Big Four accounting / audit firms worldwide from 2009 to 2022 (in billion U.S. dollars) (2023). Statista Research Department. Available at: https://www.statista.com/statistics/473959/big-four-accounting-firms-global-combined-revenue/

- GDP. World Bank Open Data. Available at: https://data.worldbank.org/indicator/NY.GDP.MKTP.CD

- Big 4 Accounting Firms 2023 Layoffs. Available at: https://big4accountingfirms.com/the-blog/big-4-accounting-firms-2023-layoffs/

- Povoienna vidbudova: doslidzhennia dosvidu ta potochnoho stanu. Available at: https://kpmg.com/ua/uk/home/insights/2022/12/post-war-reconstruction-of-economy-case-studies.html

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2023 Tamara Gordieieva, Arutiun Tsaturian

This work is licensed under a Creative Commons Attribution 4.0 International License.

The consolidation and conditions for the transfer of copyright (identification of authorship) is carried out in the License Agreement. In particular, the authors reserve the right to the authorship of their manuscript and transfer the first publication of this work to the journal under the terms of the Creative Commons CC BY license. At the same time, they have the right to conclude on their own additional agreements concerning the non-exclusive distribution of the work in the form in which it was published by this journal, but provided that the link to the first publication of the article in this journal is preserved.