Глобальні напрямки досліджень інтегрованої звітності з аналізом методу мережевих карт

DOI:

https://doi.org/10.15587/1729-4061.2022.265763Ключові слова:

інтегрована звітність, VOSviewer, бібліометричний аналіз, мережева візуалізація, Web of ScienceАнотація

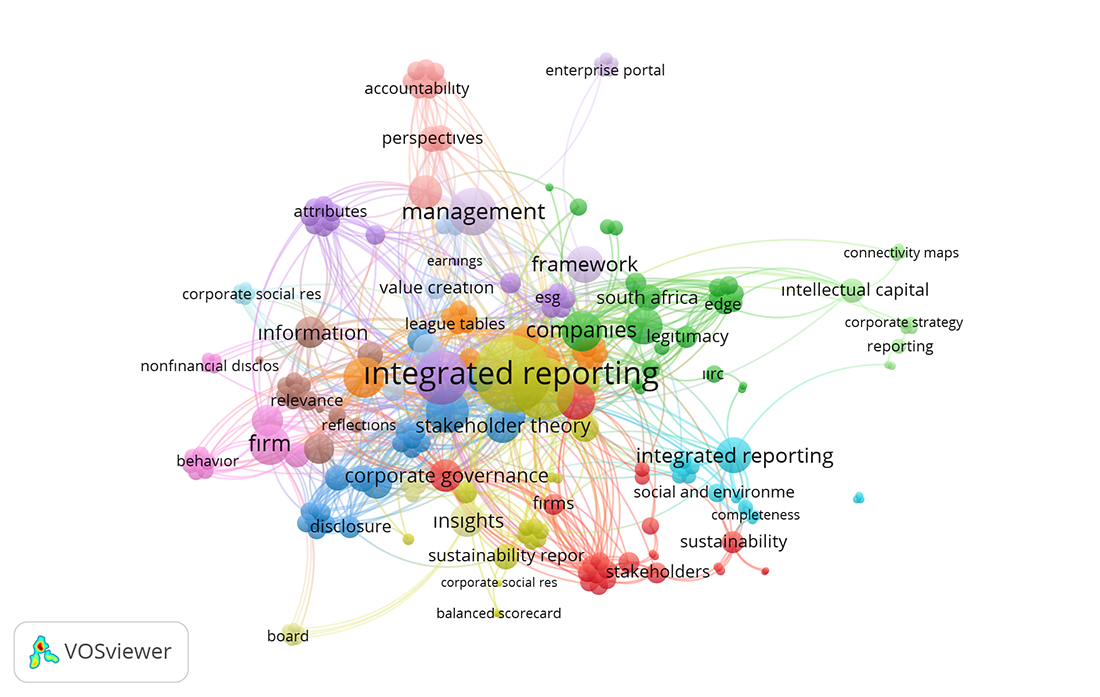

В даному дослідженні виконано систематичний аналіз глобальних напрямків досліджень, проведених у період з 1988 по 2021 рік з інтегрованої звітності, яка являє собою інструмент нефінансової звітності, що фокусується на процесі переходу від підходу за участю акціонерів до підходу за участю зацікавлених сторін та концепції створення вартості, яка спільно орієнтована на корпоративне управління, звітність та візуалізацію. Вважається, що бібліометричний аналіз академічних досліджень в області інтегрованої звітності внесе важливий внесок з точки зору виявлення того, які поняття обговорюються в літературі та який вимір взаємозв'язку. Для цього дані, отримані з бази даних Web of Science Core Collection, були проаналізовані за допомогою програмного забезпечення VOSviewer. У базі даних було отримано 462 дослідження в діапазоні дат, визначеному ключовим словом "інтегрована звітність" у категорії заголовка. Було проведено систематичний бібліометричний аналіз, який включав різні змінні, такі як кількість цитувань, провідні автори, організації, ключові слова та країни, в яких були написані статті. Згідно з результатами аналізу, трьома найбільш впливовими журналами для досліджень в області інтегрованої звітності є Meditari Accountancy Research, Journal of Intellectual Capital та Sustainability. Переважна більшість досліджень була опублікована англійською мовою. Трьома найбільш публікованими авторами є Raimo Nicola, Vitolla Filippo і Dumay John. Найбільш впливовими установами є Бухарестський університет економічних досліджень, університет Жана Моне та університет Маккуорі. Отримані результати допоможуть дослідникам у цій галузі зрозуміти загальну тенденцію, актуальність та ефективність змінних у глобальних дослідженнях інтегрованої звітності, а також слугуватимуть керівництвом для подальших досліджень.

Посилання

- Adams, C. A. (2015). The International Integrated Reporting Council: A call to action. Critical Perspectives on Accounting, 27, 23–28. doi: https://doi.org/10.1016/j.cpa.2014.07.001

- Brown, J., Dillard, J. (2014). Integrated reporting: On the need for broadening out and opening up. Accounting, Auditing & Accountability Journal, 27 (7), 1120–1156. doi: https://doi.org/10.1108/aaaj-04-2013-1313

- van Eck, N. J., Waltman, L. (2017). Citation-based clustering of publications using CitNetExplorer and VOSviewer. Scientometrics, 111 (2), 1053–1070. doi: https://doi.org/10.1007/s11192-017-2300-7

- Wang, Q. (2018). Distribution features and intellectual structures of digital humanities. Journal of Documentation, 74 (1), 223–246. doi: https://doi.org/10.1108/jd-05-2017-0076

- Bhattacharya, S., Basu, P. K. (1998). Mapping a research area at the micro level using co-word analysis. Scientometrics, 43 (3), 359–372. doi: https://doi.org/10.1007/bf02457404

- Cerbone, D., Maroun, W. (2020). Materiality in an integrated reporting setting: Insights using an institutional logics framework. The British Accounting Review, 52 (3), 100876. doi: https://doi.org/10.1016/j.bar.2019.100876

- Ciubotariu, M.-S., Socoliuc, M., Grosu, V., Mihaila, S., Cosmulese, C. G. C. (2021). Modeling the relationship between integrated reporting quality and sustainable business development. Journal of Business Economics and Management, 22 (6), 1476–1491. doi: https://doi.org/10.3846/jbem.2021.15601

- Ozkose, H., Gencer, C. (2017). Bibliometric analysis and mapping of management information systems field. Gazi University Journal of Science, 30 (4), 356–371. Available at: https://dergipark.org.tr/en/pub/gujs/issue/32802/283182#article_cite

- José de Oliveira, O., Francisco da Silva, F., Juliani, F., César Ferreira Motta Barbosa, L., Vieira Nunhes, T. (2019). Bibliometric Method for Mapping the State-of-the-Art and Identifying Research Gaps and Trends in Literature: An Essential Instrument to Support the Development of Scientific Projects. Scientometrics Recent Advances. doi: https://doi.org/10.5772/intechopen.85856

- Dumay, J., Bernardi, C., Guthrie, J., Demartini, P. (2016). Integrated reporting: A structured literature review. Accounting Forum, 40 (3), 166–185. doi: https://doi.org/10.1016/j.accfor.2016.06.001

- Maier, D., Maier, A., Așchilean, I., Anastasiu, L., Gavriș, O. (2020). The Relationship between Innovation and Sustainability: A Bibliometric Review of the Literature. Sustainability, 12 (10), 4083. doi: https://doi.org/10.3390/su12104083

- de Villiers, C., Sharma, U. (2020). A critical reflection on the future of financial, intellectual capital, sustainability and integrated reporting. Critical Perspectives on Accounting, 70, 101999. doi: https://doi.org/10.1016/j.cpa.2017.05.003

- Moral-Muñoz, J. A., Herrera-Viedma, E., Santisteban-Espejo, A., Cobo, M. J. (2020). Software tools for conducting bibliometric analysis in science: An up-to-date review. El Profesional de La Información, 29 (1). doi: https://doi.org/10.3145/epi.2020.ene.03

- Doleck, T., Lajoie, S. (2017). Social networking and academic performance: A review. Education and Information Technologies, 23 (1), 435–465. doi: https://doi.org/10.1007/s10639-017-9612-3

- Shanti, S., Tjahjadi, B., Narsa, I. M. (2020). Integrated Reporting’s Impact on Corporate Governance: Study in Asean Capital Market. Assets: Jurnal Akuntansi Dan Pendidikan, 9 (1), 1. doi: https://doi.org/10.25273/jap.v9i1.5383

- Flower, J. (2015). The International Integrated Reporting Council: A story of failure. Critical Perspectives on Accounting, 27, 1–17. doi: https://doi.org/10.1016/j.cpa.2014.07.002

- García-Sánchez, I.-M., Rodríguez-Ariza, L., Frías-Aceituno, J.-V. (2013). The cultural system and integrated reporting. International Business Review, 22 (5), 828–838. doi: https://doi.org/10.1016/j.ibusrev.2013.01.007

- Mohammad, N. (2019). Integrated Reporting Practice and Disclosure in Bangladesh’s Banking Sectors. Indonesian Journal of Sustainability Accounting and Management, 3 (2), 147. doi: https://doi.org/10.28992/ijsam.v3i2.91

- Katoch, R. (2022). IoT research in supply chain management and logistics: A bibliometric analysis using vosviewer software. Materials Today: Proceedings, 56, 2505–2515. doi: https://doi.org/10.1016/j.matpr.2021.08.272

- Cash-Gibson, L., Rojas-Gualdrón, D. F., Pericàs, J. M., Benach, J. (2018). Inequalities in global health inequalities research: A 50-year bibliometric analysis (1966-2015). PLOS ONE, 13 (1), e0191901. doi: https://doi.org/10.1371/journal.pone.0191901

- Iredele, O. O. (2019). Examining the association between quality of integrated reports and corporate characteristics. Heliyon, 5 (7), e01932. doi: https://doi.org/10.1016/j.heliyon.2019.e01932

- Sengupta, I. N. (1992). Bibliometrics, Informetrics, Scientometrics and Librametrics: An Overview. Libri, 42 (2). doi: https://doi.org/10.1515/libr.1992.42.2.75

- Rahman, M., Haque, T. L., Fukui, T. (2005). Research Articles Published in Clinical Radiology Journals: Trend of Contribution from Different Countries1. Academic Radiology, 12 (7), 825–829. doi: https://doi.org/10.1016/j.acra.2005.03.061

- Mascarenhas, C., Ferreira, J. J., Marques, C. (2018). University–industry cooperation: A systematic literature review and research agenda. Science and Public Policy, 45 (5), 708–718. doi: https://doi.org/10.1093/scipol/scy003

- Marcucci, G., Ciarapica, F., Poler, R., Sanchis, R. (2021). A Bibliometric Analysis of the Emerging Trends in Silver Economy. IFAC-PapersOnLine, 54 (1), 936–941. doi: https://doi.org/10.1016/j.ifacol.2021.08.190

- Frias-Aceituno, J. V., Rodríguez-Ariza, L., García-Sánchez, I. M. (2013). Is integrated reporting determined by a country's legal system? An exploratory study. Journal of Cleaner Production, 44, 45–55. doi: https://doi.org/10.1016/j.jclepro.2012.12.006

- Fang, Y., Yin, J., Wu, B. (2017). Climate change and tourism: a scientometric analysis using CiteSpace. Journal of Sustainable Tourism, 26 (1), 108–126. doi: https://doi.org/10.1080/09669582.2017.1329310

- Obeng, V. A., Ahmed, K., Miglani, S. (2020). Integrated reporting and earnings quality: The moderating effect of agency costs. Pacific-Basin Finance Journal, 60, 101285. doi: https://doi.org/10.1016/j.pacfin.2020.101285

- Sokil, O. (2020). Accounting and Analytical Support for Cost and Value Added Management: The Way to Sustainable Development. Accounting and Finance, 1 (87), 59–68. doi: https://doi.org/10.33146/2307-9878-2020-1(87)-59-68

- Goyal, N. (2017). A “review” of policy sciences: bibliometric analysis of authors, references, and topics during 1970–2017. Policy Sciences, 50 (4), 527–537. doi: https://doi.org/10.1007/s11077-017-9300-6

- Huang, Y., Huang, Q., Ali, S., Zhai, X., Bi, X., Liu, R. (2016). Rehabilitation using virtual reality technology: a bibliometric analysis, 1996–2015. Scientometrics, 109 (3), 1547–1559. doi: https://doi.org/10.1007/s11192-016-2117-9

- Zhou, S., Simnett, R., Green, W. (2017). Does Integrated Reporting Matter to the Capital Market? Abacus, 53 (1), 94–132. doi: https://doi.org/10.1111/abac.12104

- Xie, H., Zhang, Y., Wu, Z., Lv, T. (2020). A Bibliometric Analysis on Land Degradation: Current Status, Development, and Future Directions. Land, 9 (1), 28. doi: https://doi.org/10.3390/land9010028

- van Nunen, K., Li, J., Reniers, G., Ponnet, K. (2018). Bibliometric analysis of safety culture research. Safety Science, 108, 248–258. doi: https://doi.org/10.1016/j.ssci.2017.08.011

- Jensen, J. C., Berg, N. (2011). Determinants of Traditional Sustainability Reporting Versus Integrated Reporting. An Institutionalist Approach. Business Strategy and the Environment, 21 (5), 299–316. doi: https://doi.org/10.1002/bse.740

- Michalopoulos, A., Falagas, M. E. (2005). A Bibliometric Analysis of Global Research Production in Respiratory Medicine. Chest, 128 (6), 3993–3998. doi: https://doi.org/10.1378/chest.128.6.3993

- Stubbs, W., Higgins, C. (2014). Integrated Reporting and internal mechanisms of change. Accounting, Auditing & Accountability Journal, 27 (7), 1068–1089. doi: https://doi.org/10.1108/aaaj-03-2013-1279

- Wallin, J. A. (2005). Bibliometric methods: pitfalls and possibilities. Basic & clinical pharmacology & toxicology, 97 (5), 261–275. doi: https://doi.org/10.1111/j.1742-7843.2005.pto_139.x

- Yu, D., Wang, W., Zhang, W., Zhang, S. (2018). A Bibliometric Analysis of Research on Multiple Criteria Decision Making. Current Science, 114 (04), 747. doi: https://doi.org/10.18520/cs/v114/i04/747-758

- Zhong, S., Geng, Y., Liu, W., Gao, C., Chen, W. (2016). A bibliometric review on natural resource accounting during 1995–2014. Journal of Cleaner Production, 139, 122–132. doi: https://doi.org/10.1016/j.jclepro.2016.08.039

- Kemeç, A. (2022). Analysis of smart city global research trends with network map technique. Management Research & Practice, 14 (2), 46–59.

##submission.downloads##

Опубліковано

Як цитувати

Номер

Розділ

Ліцензія

Авторське право (c) 2022 Aysenur Tarakcioglu Altinay

Ця робота ліцензується відповідно до Creative Commons Attribution 4.0 International License.

Закріплення та умови передачі авторських прав (ідентифікація авторства) здійснюється у Ліцензійному договорі. Зокрема, автори залишають за собою право на авторство свого рукопису та передають журналу право першої публікації цієї роботи на умовах ліцензії Creative Commons CC BY. При цьому вони мають право укладати самостійно додаткові угоди, що стосуються неексклюзивного поширення роботи у тому вигляді, в якому вона була опублікована цим журналом, але за умови збереження посилання на першу публікацію статті в цьому журналі.

Ліцензійний договір – це документ, в якому автор гарантує, що володіє усіма авторськими правами на твір (рукопис, статтю, тощо).

Автори, підписуючи Ліцензійний договір з ПП «ТЕХНОЛОГІЧНИЙ ЦЕНТР», мають усі права на подальше використання свого твору за умови посилання на наше видання, в якому твір опублікований. Відповідно до умов Ліцензійного договору, Видавець ПП «ТЕХНОЛОГІЧНИЙ ЦЕНТР» не забирає ваші авторські права та отримує від авторів дозвіл на використання та розповсюдження публікації через світові наукові ресурси (власні електронні ресурси, наукометричні бази даних, репозитарії, бібліотеки тощо).

За відсутності підписаного Ліцензійного договору або за відсутністю вказаних в цьому договорі ідентифікаторів, що дають змогу ідентифікувати особу автора, редакція не має права працювати з рукописом.

Важливо пам’ятати, що існує і інший тип угоди між авторами та видавцями – коли авторські права передаються від авторів до видавця. В такому разі автори втрачають права власності на свій твір та не можуть його використовувати в будь-який спосіб.