Global research trends of ıntegrated reportıng wıth network map technıque analysıs

DOI:

https://doi.org/10.15587/1729-4061.2022.265763Keywords:

integrated reporting, VOSviewer, bibliometrics analysis, network visualization, Web of ScienceAbstract

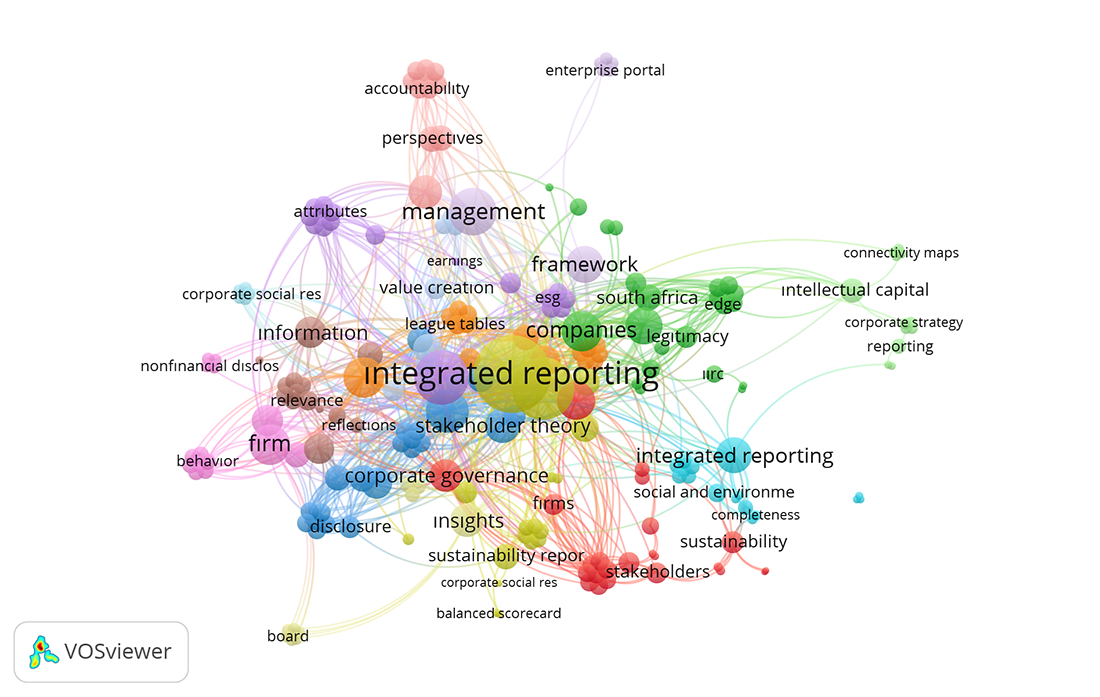

In this study, a systematic analysis of the global trends of the studies carried out between 1988‒2021 on integrated reporting, which is a non-financial reporting tool that focuses on the process evolving from the shareholder approach to the stakeholder approach and the concept of value creation, which is jointly focused on corporate governance and reporting and visualization is performed. It is thought that bibliometric analysis of academic studies in the field of integrated reporting will make important contributions in terms of revealing which concepts are discussed in the literature and which relationship dimension. For this purpose, the data obtained from the Web of Science Core Collection Database were analyzed with the VOSviewer software. In the database, 462 studies were reached in the date range determined by the keyword “integrated reporting” in the title category. A systematic bibliometric analysis was conducted that included different variables such as citation counts, leading authors, organizations, keywords, and countries where the articles were written. According to the findings from the analysis, the three most influential journals for integrated reporting research are Meditari Accountancy Research, Journal of Intellectual Capital, and Sustainability. The vast majority of studies were published in the English language. The three most published authors are Raimo Nicola, Vitolla Filippo and Dumay John. The most influential institutions are Bucharest University of Economic Studies, Lum Jean Monnet University and Macquarie University. The findings will help researchers in the field understand the overall trend, relevance and performance of variables in globally integrated reporting research, and will provide guidelines for further research

References

- Adams, C. A. (2015). The International Integrated Reporting Council: A call to action. Critical Perspectives on Accounting, 27, 23–28. doi: https://doi.org/10.1016/j.cpa.2014.07.001

- Brown, J., Dillard, J. (2014). Integrated reporting: On the need for broadening out and opening up. Accounting, Auditing & Accountability Journal, 27 (7), 1120–1156. doi: https://doi.org/10.1108/aaaj-04-2013-1313

- van Eck, N. J., Waltman, L. (2017). Citation-based clustering of publications using CitNetExplorer and VOSviewer. Scientometrics, 111 (2), 1053–1070. doi: https://doi.org/10.1007/s11192-017-2300-7

- Wang, Q. (2018). Distribution features and intellectual structures of digital humanities. Journal of Documentation, 74 (1), 223–246. doi: https://doi.org/10.1108/jd-05-2017-0076

- Bhattacharya, S., Basu, P. K. (1998). Mapping a research area at the micro level using co-word analysis. Scientometrics, 43 (3), 359–372. doi: https://doi.org/10.1007/bf02457404

- Cerbone, D., Maroun, W. (2020). Materiality in an integrated reporting setting: Insights using an institutional logics framework. The British Accounting Review, 52 (3), 100876. doi: https://doi.org/10.1016/j.bar.2019.100876

- Ciubotariu, M.-S., Socoliuc, M., Grosu, V., Mihaila, S., Cosmulese, C. G. C. (2021). Modeling the relationship between integrated reporting quality and sustainable business development. Journal of Business Economics and Management, 22 (6), 1476–1491. doi: https://doi.org/10.3846/jbem.2021.15601

- Ozkose, H., Gencer, C. (2017). Bibliometric analysis and mapping of management information systems field. Gazi University Journal of Science, 30 (4), 356–371. Available at: https://dergipark.org.tr/en/pub/gujs/issue/32802/283182#article_cite

- José de Oliveira, O., Francisco da Silva, F., Juliani, F., César Ferreira Motta Barbosa, L., Vieira Nunhes, T. (2019). Bibliometric Method for Mapping the State-of-the-Art and Identifying Research Gaps and Trends in Literature: An Essential Instrument to Support the Development of Scientific Projects. Scientometrics Recent Advances. doi: https://doi.org/10.5772/intechopen.85856

- Dumay, J., Bernardi, C., Guthrie, J., Demartini, P. (2016). Integrated reporting: A structured literature review. Accounting Forum, 40 (3), 166–185. doi: https://doi.org/10.1016/j.accfor.2016.06.001

- Maier, D., Maier, A., Așchilean, I., Anastasiu, L., Gavriș, O. (2020). The Relationship between Innovation and Sustainability: A Bibliometric Review of the Literature. Sustainability, 12 (10), 4083. doi: https://doi.org/10.3390/su12104083

- de Villiers, C., Sharma, U. (2020). A critical reflection on the future of financial, intellectual capital, sustainability and integrated reporting. Critical Perspectives on Accounting, 70, 101999. doi: https://doi.org/10.1016/j.cpa.2017.05.003

- Moral-Muñoz, J. A., Herrera-Viedma, E., Santisteban-Espejo, A., Cobo, M. J. (2020). Software tools for conducting bibliometric analysis in science: An up-to-date review. El Profesional de La Información, 29 (1). doi: https://doi.org/10.3145/epi.2020.ene.03

- Doleck, T., Lajoie, S. (2017). Social networking and academic performance: A review. Education and Information Technologies, 23 (1), 435–465. doi: https://doi.org/10.1007/s10639-017-9612-3

- Shanti, S., Tjahjadi, B., Narsa, I. M. (2020). Integrated Reporting’s Impact on Corporate Governance: Study in Asean Capital Market. Assets: Jurnal Akuntansi Dan Pendidikan, 9 (1), 1. doi: https://doi.org/10.25273/jap.v9i1.5383

- Flower, J. (2015). The International Integrated Reporting Council: A story of failure. Critical Perspectives on Accounting, 27, 1–17. doi: https://doi.org/10.1016/j.cpa.2014.07.002

- García-Sánchez, I.-M., Rodríguez-Ariza, L., Frías-Aceituno, J.-V. (2013). The cultural system and integrated reporting. International Business Review, 22 (5), 828–838. doi: https://doi.org/10.1016/j.ibusrev.2013.01.007

- Mohammad, N. (2019). Integrated Reporting Practice and Disclosure in Bangladesh’s Banking Sectors. Indonesian Journal of Sustainability Accounting and Management, 3 (2), 147. doi: https://doi.org/10.28992/ijsam.v3i2.91

- Katoch, R. (2022). IoT research in supply chain management and logistics: A bibliometric analysis using vosviewer software. Materials Today: Proceedings, 56, 2505–2515. doi: https://doi.org/10.1016/j.matpr.2021.08.272

- Cash-Gibson, L., Rojas-Gualdrón, D. F., Pericàs, J. M., Benach, J. (2018). Inequalities in global health inequalities research: A 50-year bibliometric analysis (1966-2015). PLOS ONE, 13 (1), e0191901. doi: https://doi.org/10.1371/journal.pone.0191901

- Iredele, O. O. (2019). Examining the association between quality of integrated reports and corporate characteristics. Heliyon, 5 (7), e01932. doi: https://doi.org/10.1016/j.heliyon.2019.e01932

- Sengupta, I. N. (1992). Bibliometrics, Informetrics, Scientometrics and Librametrics: An Overview. Libri, 42 (2). doi: https://doi.org/10.1515/libr.1992.42.2.75

- Rahman, M., Haque, T. L., Fukui, T. (2005). Research Articles Published in Clinical Radiology Journals: Trend of Contribution from Different Countries1. Academic Radiology, 12 (7), 825–829. doi: https://doi.org/10.1016/j.acra.2005.03.061

- Mascarenhas, C., Ferreira, J. J., Marques, C. (2018). University–industry cooperation: A systematic literature review and research agenda. Science and Public Policy, 45 (5), 708–718. doi: https://doi.org/10.1093/scipol/scy003

- Marcucci, G., Ciarapica, F., Poler, R., Sanchis, R. (2021). A Bibliometric Analysis of the Emerging Trends in Silver Economy. IFAC-PapersOnLine, 54 (1), 936–941. doi: https://doi.org/10.1016/j.ifacol.2021.08.190

- Frias-Aceituno, J. V., Rodríguez-Ariza, L., García-Sánchez, I. M. (2013). Is integrated reporting determined by a country's legal system? An exploratory study. Journal of Cleaner Production, 44, 45–55. doi: https://doi.org/10.1016/j.jclepro.2012.12.006

- Fang, Y., Yin, J., Wu, B. (2017). Climate change and tourism: a scientometric analysis using CiteSpace. Journal of Sustainable Tourism, 26 (1), 108–126. doi: https://doi.org/10.1080/09669582.2017.1329310

- Obeng, V. A., Ahmed, K., Miglani, S. (2020). Integrated reporting and earnings quality: The moderating effect of agency costs. Pacific-Basin Finance Journal, 60, 101285. doi: https://doi.org/10.1016/j.pacfin.2020.101285

- Sokil, O. (2020). Accounting and Analytical Support for Cost and Value Added Management: The Way to Sustainable Development. Accounting and Finance, 1 (87), 59–68. doi: https://doi.org/10.33146/2307-9878-2020-1(87)-59-68

- Goyal, N. (2017). A “review” of policy sciences: bibliometric analysis of authors, references, and topics during 1970–2017. Policy Sciences, 50 (4), 527–537. doi: https://doi.org/10.1007/s11077-017-9300-6

- Huang, Y., Huang, Q., Ali, S., Zhai, X., Bi, X., Liu, R. (2016). Rehabilitation using virtual reality technology: a bibliometric analysis, 1996–2015. Scientometrics, 109 (3), 1547–1559. doi: https://doi.org/10.1007/s11192-016-2117-9

- Zhou, S., Simnett, R., Green, W. (2017). Does Integrated Reporting Matter to the Capital Market? Abacus, 53 (1), 94–132. doi: https://doi.org/10.1111/abac.12104

- Xie, H., Zhang, Y., Wu, Z., Lv, T. (2020). A Bibliometric Analysis on Land Degradation: Current Status, Development, and Future Directions. Land, 9 (1), 28. doi: https://doi.org/10.3390/land9010028

- van Nunen, K., Li, J., Reniers, G., Ponnet, K. (2018). Bibliometric analysis of safety culture research. Safety Science, 108, 248–258. doi: https://doi.org/10.1016/j.ssci.2017.08.011

- Jensen, J. C., Berg, N. (2011). Determinants of Traditional Sustainability Reporting Versus Integrated Reporting. An Institutionalist Approach. Business Strategy and the Environment, 21 (5), 299–316. doi: https://doi.org/10.1002/bse.740

- Michalopoulos, A., Falagas, M. E. (2005). A Bibliometric Analysis of Global Research Production in Respiratory Medicine. Chest, 128 (6), 3993–3998. doi: https://doi.org/10.1378/chest.128.6.3993

- Stubbs, W., Higgins, C. (2014). Integrated Reporting and internal mechanisms of change. Accounting, Auditing & Accountability Journal, 27 (7), 1068–1089. doi: https://doi.org/10.1108/aaaj-03-2013-1279

- Wallin, J. A. (2005). Bibliometric methods: pitfalls and possibilities. Basic & clinical pharmacology & toxicology, 97 (5), 261–275. doi: https://doi.org/10.1111/j.1742-7843.2005.pto_139.x

- Yu, D., Wang, W., Zhang, W., Zhang, S. (2018). A Bibliometric Analysis of Research on Multiple Criteria Decision Making. Current Science, 114 (04), 747. doi: https://doi.org/10.18520/cs/v114/i04/747-758

- Zhong, S., Geng, Y., Liu, W., Gao, C., Chen, W. (2016). A bibliometric review on natural resource accounting during 1995–2014. Journal of Cleaner Production, 139, 122–132. doi: https://doi.org/10.1016/j.jclepro.2016.08.039

- Kemeç, A. (2022). Analysis of smart city global research trends with network map technique. Management Research & Practice, 14 (2), 46–59.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2022 Aysenur Tarakcioglu Altinay

This work is licensed under a Creative Commons Attribution 4.0 International License.

The consolidation and conditions for the transfer of copyright (identification of authorship) is carried out in the License Agreement. In particular, the authors reserve the right to the authorship of their manuscript and transfer the first publication of this work to the journal under the terms of the Creative Commons CC BY license. At the same time, they have the right to conclude on their own additional agreements concerning the non-exclusive distribution of the work in the form in which it was published by this journal, but provided that the link to the first publication of the article in this journal is preserved.

A license agreement is a document in which the author warrants that he/she owns all copyright for the work (manuscript, article, etc.).

The authors, signing the License Agreement with TECHNOLOGY CENTER PC, have all rights to the further use of their work, provided that they link to our edition in which the work was published.

According to the terms of the License Agreement, the Publisher TECHNOLOGY CENTER PC does not take away your copyrights and receives permission from the authors to use and dissemination of the publication through the world's scientific resources (own electronic resources, scientometric databases, repositories, libraries, etc.).

In the absence of a signed License Agreement or in the absence of this agreement of identifiers allowing to identify the identity of the author, the editors have no right to work with the manuscript.

It is important to remember that there is another type of agreement between authors and publishers – when copyright is transferred from the authors to the publisher. In this case, the authors lose ownership of their work and may not use it in any way.