Development of a multidimensional framework for audit efficiency enhancement based on digital technologies and predictive data analytics

DOI:

https://doi.org/10.15587/1729-4061.2026.364574Keywords:

audit optimization, digital technologies, data analytics, audit efficiency, information systemsAbstract

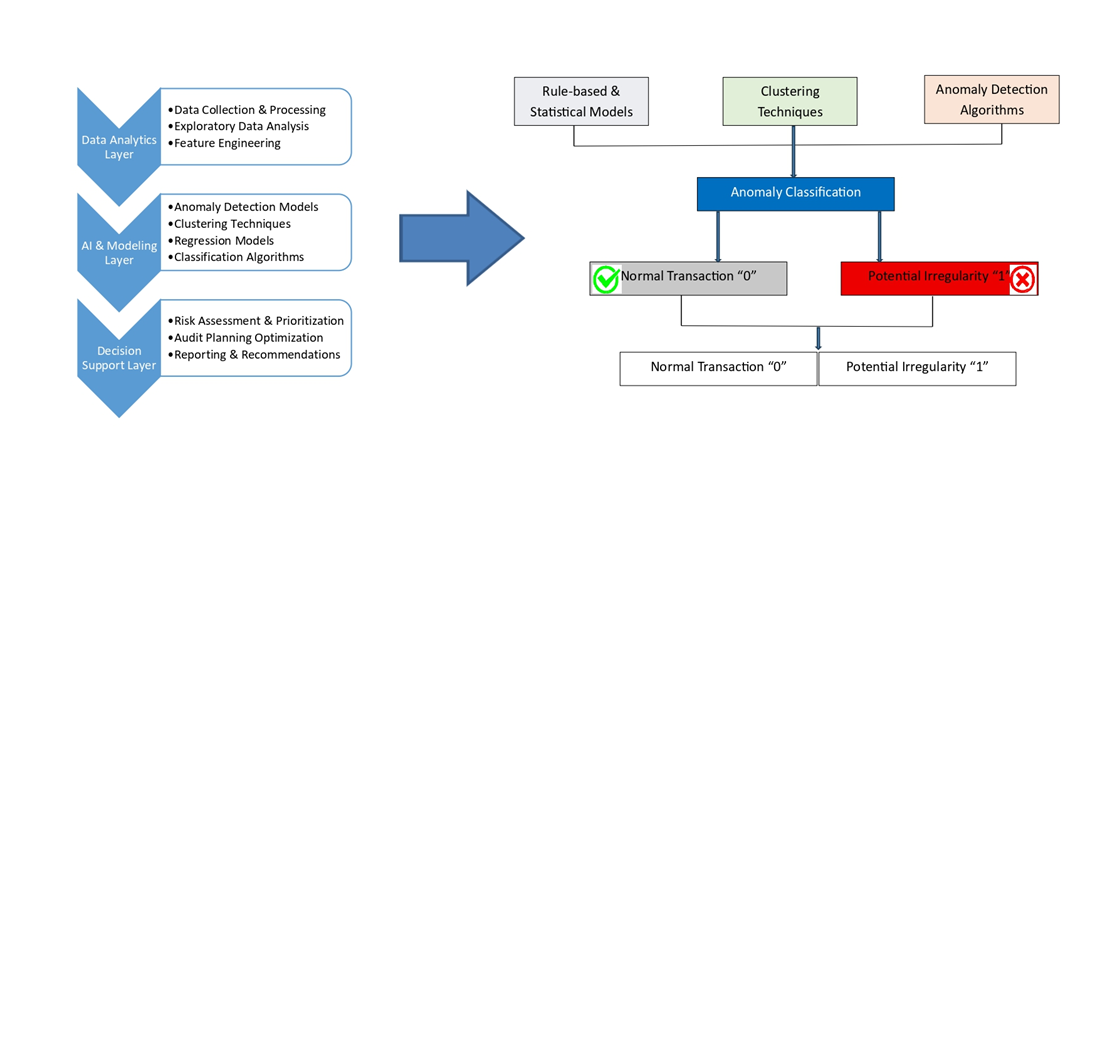

The object of study is the modern audit practice against the background of digital transformation of the mechanisms of financial management and supervision in corporate structures. The problem that needed to be addressed is the inefficiency and frequent errors of the traditional audit procedures, based on manual work with large volumes of data and sampling. As a result of the performed study, it can be noted that the usage of information technology and advanced data analytics leads to higher effectiveness by changing the traditional procedure of audit sampling for the continuous monitoring of all audit populations. It appears that systematic analysis and implementation of analytical algorithms increase the quality of assessing risks and identifying anomalies. The results obtained can be explained by the fact that the usage of digital technology eliminates all cognitive restrictions of human beings and allows finding out all anomalies at once. Among the characteristics of the results that helped solve the problem is a formalized multi-model risk minimization framework. Optimization of operations was implemented trough synthesizing the functions of regression, clustering (PAM), and Isolation Forest sub-models, regulated by the set of thresholds (τ*) and optimized weights (ωm) that minimize classification entropy. Empirical testing of the proposed approach using the real transaction entries database (n = 12 450) showed an increase in effectiveness from the base level of 65% to 88% in the framework. Specific features is associated with the synthesis of various mathematical vectors in the constrained operational pipeline based on limited time resources. Practical applications cover internal and external audit departments of large companies

References

- Brynjolfsson, E., McAfee, A. (2017). The business of artificial intelligence. Harvard Business Review. Available at: https://hbr.org/2017/07/the-business-of-artificial-intelligence

- Chen, H., Chiang, R. H. L., Storey, V. C. (2012). Business Intelligence and Analytics: From Big Data to Big Impact. MIS Quarterly, 36 (4), 1165–1188. https://doi.org/10.2307/41703503

- Sutton, S. G., Holt, M., Arnold, V. (2016). “The reports of my death are greatly exaggerated” – Artificial intelligence research in accounting. International Journal of Accounting Information Systems, 22, 60–73. https://doi.org/10.1016/j.accinf.2016.07.005

- Appelbaum, D., Kogan, A., Vasarhelyi, M. A. (2017). Big Data and Analytics in the Modern Audit Engagement: Research Needs. Auditing: A Journal of Practice & Theory, 36(4), 1–27. https://doi.org/10.2308/ajpt-51684

- Alles, M., Gray, G. L. (2016). Incorporating big data in audits: Identifying inhibitors and a research agenda to address those inhibitors. International Journal of Accounting Information Systems, 22, 44–59. https://doi.org/10.1016/j.accinf.2016.07.004

- Alles, M. G., Kogan, A., Vasarhelyi, M. A. (2008). Putting Continuous Auditing Theory into Practice: Lessons from Two Pilot Implementations. Journal of Information Systems, 22 (2), 195–214. https://doi.org/10.2308/jis.2008.22.2.195

- Alles, M., Brennan, G., Kogan, A., Vasarhelyi, M. A. (2006). Continuous monitoring of business process controls: A pilot implementation of a continuous auditing system at Siemens. International Journal of Accounting Information Systems, 7 (2), 137–161. https://doi.org/10.1016/j.accinf.2005.10.004

- Kokina, J., Davenport, T. H. (2017). The Emergence of Artificial Intelligence: How Automation is Changing Auditing. Journal of Emerging Technologies in Accounting, 14 (1), 115–122. https://doi.org/10.2308/jeta-51730

- IAASB. Available at: https://www.iaasb.org/

- ACCA. Available at: https://www.accaglobal.com

- Vasarhelyi, M. A., Kogan, A., Tuttle, B. M. (2015). Big Data in Accounting: An Overview. Accounting Horizons, 29 (2), 381–396. https://doi.org/10.2308/acch-51071

- Davenport, T. H., Ronanki, R. (2018). Artificial intelligence for the real world. Harvard Business Review. Available at: https://hbr.org/2018/01/artificial-intelligence-for-the-real-world

- Issa, H., Sun, T., Vasarhelyi, M. A. (2016). Research Ideas for Artificial Intelligence in Auditing: The Formalization of Audit and Workforce Supplementation. Journal of Emerging Technologies in Accounting, 13 (2), 1–20. https://doi.org/10.2308/jeta-10511

- Gepp, A., Linnenluecke, M. K., O’Neill, T. J., Smith, T. (2018). Big data techniques in auditing research and practice: Current trends and future opportunities. Journal of Accounting Literature, 40 (1), 102–115. https://doi.org/10.1016/j.acclit.2017.05.003

- Hadzhi, K. M., Vali, G. X., Viladdin, M. A., Cemil, K. I., Ali, Y. S., Fizuli, H. Z., Tahir, P. A. (2024). Marketing strategy as a key factor of innovative products’ market development. Journal of Law and Sustainable Development, 12 (7), e3755. https://doi.org/10.55908/sdgs.v12i7.3755

- Mammadov, J., Huseynov, Y., Ahmadova, M., Mammadova, G., Askerov, A. (2025). Developing a marketing strategy for efficient management of the information environment of the technology park. Eastern-European Journal of Enterprise Technologies, 3 (13 (135)), 26–34. https://doi.org/10.15587/1729-4061.2025.330483

- IFAC. Available at: https://www.ifac.org

- Chakraborty, V., Chiu, V., Vasarhelyi, M. (2014). Automatic classification of accounting literature. International Journal of Accounting Information Systems, 15(2), 122–148. https://doi.org/10.1016/j.accinf.2014.01.001

- Earley, C. E. (2015). Data analytics in auditing: Opportunities and challenges. Business Horizons, 58 (5), 493–500. https://doi.org/10.1016/j.bushor.2015.05.002

- PwC. Available at: https://www.pwc.com

- Deloitte. Available at: https://www.deloitte.com

- OECD. Available at: https://www.oecd.org

- KPMG. Available at: https://www.kpmg.com

- Brown-Liburd, H., Issa, H., Lombardi, D. (2015). Behavioral Implications of Big Data’s Impact on Audit Judgment and Decision Making and Future Research Directions. Accounting Horizons, 29 (2), 451–468. https://doi.org/10.2308/acch-51023

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2026 Minura Karimova, Fazil Karimov, Matanat Ahmadova, Xayyam Cavadzada, Aytan Nadirova, Xatira Qurbanova, Surayya Ismayilova

This work is licensed under a Creative Commons Attribution 4.0 International License.

The consolidation and conditions for the transfer of copyright (identification of authorship) is carried out in the License Agreement. In particular, the authors reserve the right to the authorship of their manuscript and transfer the first publication of this work to the journal under the terms of the Creative Commons CC BY license. At the same time, they have the right to conclude on their own additional agreements concerning the non-exclusive distribution of the work in the form in which it was published by this journal, but provided that the link to the first publication of the article in this journal is preserved.

A license agreement is a document in which the author warrants that he/she owns all copyright for the work (manuscript, article, etc.).

The authors, signing the License Agreement with TECHNOLOGY CENTER PC, have all rights to the further use of their work, provided that they link to our edition in which the work was published.

According to the terms of the License Agreement, the Publisher TECHNOLOGY CENTER PC does not take away your copyrights and receives permission from the authors to use and dissemination of the publication through the world's scientific resources (own electronic resources, scientometric databases, repositories, libraries, etc.).

In the absence of a signed License Agreement or in the absence of this agreement of identifiers allowing to identify the identity of the author, the editors have no right to work with the manuscript.

It is important to remember that there is another type of agreement between authors and publishers – when copyright is transferred from the authors to the publisher. In this case, the authors lose ownership of their work and may not use it in any way.