Генерування машинозчитуваних звітів у розрізі країн за допомогою великих мовних моделей

DOI:

https://doi.org/10.15587/1729-4061.2025.337405Ключові слова:

трансфертне ціноутворення, трансфертна документація, великі мовні моделі, генерування XMLАнотація

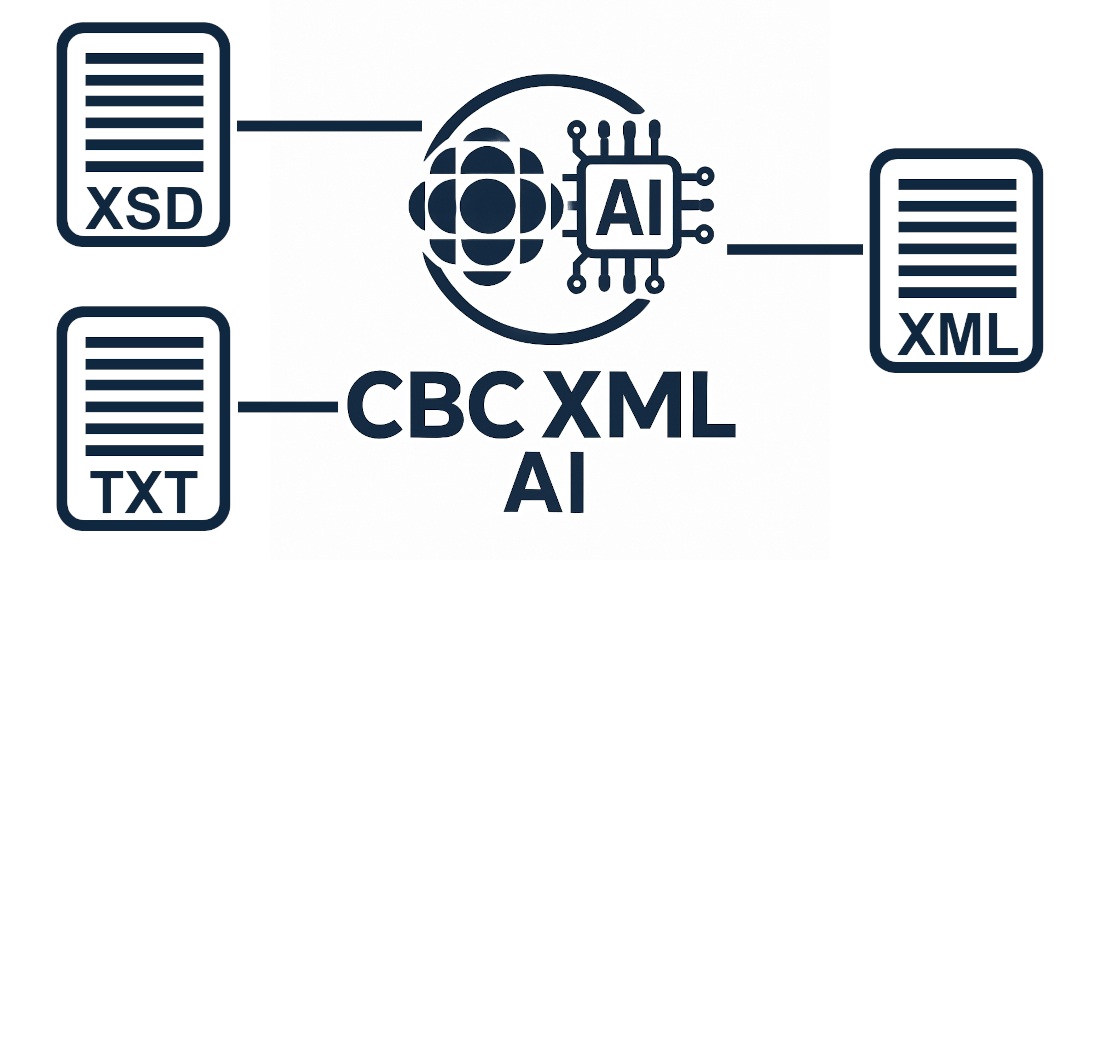

Об’єктом даного дослідження є процес генерування машинозчитуваних звітів у розрізі країн у форматі XML за допомогою великих мовних моделей. Проблемою, що вирішується у даному дослідженні, є поточна залежність процесу генерування цих звітів від спеціалізованого програмного забезпечення, що призводить до додаткових фінансових витрат.

Проведені дослідження та аналіз ефективності загальнодоступних великих мовних моделей для генерування звітів у розрізі країн з новими даними показали високі результати за умови надання моделі прикладу такого генерування. Три великі мовні моделі із дев’яти досліджених показали результати, наближені до ідеальних (що отримуються ручною підготовкою або спеціалізованими системами), а саме 96 балів із 100 за розробленою методикою оцінювання. Ще чотири досліджених моделі показали дещо нижчу ефективність, але її рівень також достатній для застосування на практиці. При цьому, отримана середня вартість генерування одного звіту (4,2 центи США) є значно меншою, ніж у випадку використання спеціалізованих систем. Стосовно ефективності великих мовних моделей загального призначення для генерування звітів у розрізі країн за відсутності прикладу генерування, то вона на сьогодні є недостатньою для використання на практиці. Всі із досліджених моделей у такому випадку показали результати, наближені до 0 балів, тобто були отримані повністю некоректні звіти. Такі результати пояснюються недостатньою кількістю навчальних даних під час тренування загальнодоступних моделей.

Таким чином, загальнодоступні великі мовні моделі можуть замінити на практиці спеціалізовані програмні системи, що призначені для генерування звітів у розрізі країн у форматі XML, щонайменше у випадку генерування нових звітів

Посилання

- Yi, Z., Cao, X., Chen, Z., Li, S. (2023). Artificial Intelligence in Accounting and Finance: Challenges and Opportunities. IEEE Access, 11, 129100–129123. https://doi.org/10.1109/access.2023.3333389

- Dubey, S. S., Astvansh, V., Kopalle, P. K. (2025). Generative AI Solutions to Empower Financial Firms. Journal of Public Policy & Marketing, 44 (3), 411–435. https://doi.org/10.1177/07439156241311300

- Action Plan on Base Erosion and Profit Shifting (2013). OECD. https://doi.org/10.1787/9789264202719-en

- Dharmapala, D. (2014). What Do We Know about Base Erosion and Profit Shifting? A Review of the Empirical Literature. Fiscal Studies, 35 (4), 421–448. https://doi.org/10.1111/j.1475-5890.2014.12037.x

- Transfer Pricing Documentation and Country-by-Country Reporting, Action 13 - 2015 Final Report. In OECD/G20 Base Erosion and Profit Shifting Project (2015). OECD. https://doi.org/10.1787/9789264241480-en

- Ouelhadj, A., Bouchetara, M. (2021). Contributions of the Base Erosion and Profit Shifting BEPS Project on Transfer Pricing and Tax Avoidance. Financial Markets, Institutions and Risks, 5 (3). https://doi.org/10.21272/fmir.5(3).59-70.2021

- Country-by-Country Reporting XML Schema: User Guide for Tax Administrations. Version 2.0 (2019). Paris: OECD Publishing. Available at: http://www.oecd.org/tax/beps/country-by-country-reporting-xml-schema-user-guide-for-tax-administrations-june-2019.pdf

- Bergmann, S. (2016). Neue Verrechnungspreisdokumentationspflichten für multinationale Unternehmensgruppen. Zeitschrift für Gesellschaftsrecht und angrenzendes Steuerrecht, 148.

- Rezultaty roboty DPS shchodo podatkovoho kontroliu za transfertnym tsinoutvorenniam (2025). Kyiv. Available at: https://tax.gov.ua/data/material/000/780/912318/Dodatok_1.pdf

- Carey, A., Tanguay, B. H. (2025). How Can GenAI Improve My Transfer Pricing Process? Tax Management International Journal. Available at: https://kpmg.com/kpmg-us/content/dam/kpmg/taxnewsflash/pdf/2025/03/KPMG_GenAI_tmij_March2025_final.pdf

- Dinev, D., Wojewoda, A. (2024). Opportunities and limitations of AI in transfer pricing. International Tax Review. Available at: https://www.internationaltaxreview.com/article/2dxro1nggp5h8t2flrtog/sponsored/opportunities-and-limitations-of-ai-in-transfer-pricing

- Khalil, M. (2024). The Role of AI in Enhancing Transfer Pricing Accuracy and Efficiency. Advances in Information Technology, 7 (1), 1–11. Available at: https://acadexpinnara.com/index.php/acs/article/view/350

- Basharat, A. (2024). The Role of AI in Transfer Pricing: Transforming Global Taxation Processes. Aitoz Multidisciplinary Review, 3 (1), 254–260. Available at: https://aitozresearch.com/index.php/amr/article/view/55

- Puttaraju, K. H. (2024). Leveraging AI for Transfer Pricing Strategy Development and Execution: A Practical Approach. Interantional Journal Of Scientific Research In Engineering And Management, 08 (11), 1–6. https://doi.org/10.55041/ijsrem32711

- Moro Visconti, R. (2025). Artificial Intelligence And Transfer Pricing: A Multilayer Network Model for Compliance and Risk Mitigation. https://doi.org/10.2139/ssrn.5209028

- Beuther, A., Fettke, P., Just, V., Riedl, A. (2020). KI-Einsatz für Effizienzgewinne bei Benchmarkstudien im Bereich Transfer Pricing. beck.digitax, 5, 316–323. Available at: https://wts.com/wts.de/publications/fachbeitraege/2020/2020_05_beck_digitax_316_Beuthe_Fettke_Just_Riedl.pdf

- Beuther, A., Rombach, A., Stephan, S., Fettke, P., Köppe-Karkutsch, J., Dönnebrink, M. (2024). Künstliche Intelligenz im Steuerbereich: Innovationsstudie zum Potenzial und zur technologischen Entwicklung. KI Studie. Available at: https://wts.de/wts.de/KI%20Studie/KI-Folgestudie%202024_20240429.pdf

- Aibidia TXM: Verrechnungspreis-Management. TAXPUNK. Available at: https://taxpunk.de/tools/328/aibidia-txm/

- PwC CbC2Go: Workflow-basiertes CbC-Reporting. TAXPUNK. Available at: https://taxpunk.de/tools/65/pwc-cbc2go/

- WTS CbCR-2-XML: Umsetzung der XML-Struktur im Rahmen des CbC-Reportings. TAXPUNK. Available at: https://taxpunk.de/tools/85/wts-cbcr-2-xml/

- TPCBC: OECD konformes Country-by-Country Reporting. TAXPUNK. Available at: https://taxpunk.de/tools/318/tpcbc/

- Chiang, W., Zheng, L., Sheng, Y., Angelopoulos, A. N., Li, T., Li, D. et al. (2024). Chatbot arena: an open platform for evaluating LLMs by human preference. Proceedings of the 41st International Conference on Machine Learning, 8359–8388. Available at: https://dl.acm.org/doi/10.5555/3692070.3692401

- What's new in .NET 8 (2024). Microsoft. Available at: https://learn.microsoft.com/en-us/dotnet/core/whats-new/dotnet-8/overview

- What's new in C# 12 (2024). Microsoft. Available at: https://learn.microsoft.com/en-us/dotnet/csharp/whats-new/csharp-12

- dotnet/command-line-api at 2.0.0-beta4.22272.1. GitHub. Available at: https://github.com/dotnet/command-line-api/tree/2.0.0-beta4.22272.1

- lofcz/LlmTornado at v3.5.18. GitHub. Available at: https://github.com/lofcz/LlmTornado/tree/v3.5.18

- Communication Manual DIP Standard 2.1 BZSt. Available at: https://www.bzst.de/SharedDocs/Downloads/EN/dip_elma/Communication_Manual_DIP_Standard_2.pdf

##submission.downloads##

Опубліковано

Як цитувати

Номер

Розділ

Ліцензія

Авторське право (c) 2025 Yakiv Yusyn

Ця робота ліцензується відповідно до Creative Commons Attribution 4.0 International License.

Закріплення та умови передачі авторських прав (ідентифікація авторства) здійснюється у Ліцензійному договорі. Зокрема, автори залишають за собою право на авторство свого рукопису та передають журналу право першої публікації цієї роботи на умовах ліцензії Creative Commons CC BY. При цьому вони мають право укладати самостійно додаткові угоди, що стосуються неексклюзивного поширення роботи у тому вигляді, в якому вона була опублікована цим журналом, але за умови збереження посилання на першу публікацію статті в цьому журналі.

Ліцензійний договір – це документ, в якому автор гарантує, що володіє усіма авторськими правами на твір (рукопис, статтю, тощо).

Автори, підписуючи Ліцензійний договір з ПП «ТЕХНОЛОГІЧНИЙ ЦЕНТР», мають усі права на подальше використання свого твору за умови посилання на наше видання, в якому твір опублікований. Відповідно до умов Ліцензійного договору, Видавець ПП «ТЕХНОЛОГІЧНИЙ ЦЕНТР» не забирає ваші авторські права та отримує від авторів дозвіл на використання та розповсюдження публікації через світові наукові ресурси (власні електронні ресурси, наукометричні бази даних, репозитарії, бібліотеки тощо).

За відсутності підписаного Ліцензійного договору або за відсутністю вказаних в цьому договорі ідентифікаторів, що дають змогу ідентифікувати особу автора, редакція не має права працювати з рукописом.

Важливо пам’ятати, що існує і інший тип угоди між авторами та видавцями – коли авторські права передаються від авторів до видавця. В такому разі автори втрачають права власності на свій твір та не можуть його використовувати в будь-який спосіб.