Виявлення визначальних факторів, що впливають на поведінковий намір користувача використовувати Traveloka Paylater

DOI:

https://doi.org/10.15587/1729-4061.2023.275735Ключові слова:

комп'ютерна самоефективність, сприймана простота використання, фінансові витрати, соціальний впливАнотація

Платіжна функція paylater широко обговорюється в якості альтернативної платіжної системи, що забезпечує простоту і гнучкість при проведенні цифрових бізнес-операцій з щорічним зростанням від 28 % до 38 %. Незважаючи на популярність додатків Traveloka як найбільшої туристичної бізнес-платформи, яку завантажили понад 100 мільйонів разів, число користувачів Traveloka Paylater обмежена всього 8,6 % від загального числа користувачів. Метою цього дослідження є обговорити, які фактори впливають на поведінковий намір користувача використовувати Traveloka Paylater.

У дослідженні взяли участь 360 респондентів-користувачів Traveloka віком від 17 років, які знали про модель оплати Paylater, але ніколи не використовували Traveloka PayLater.

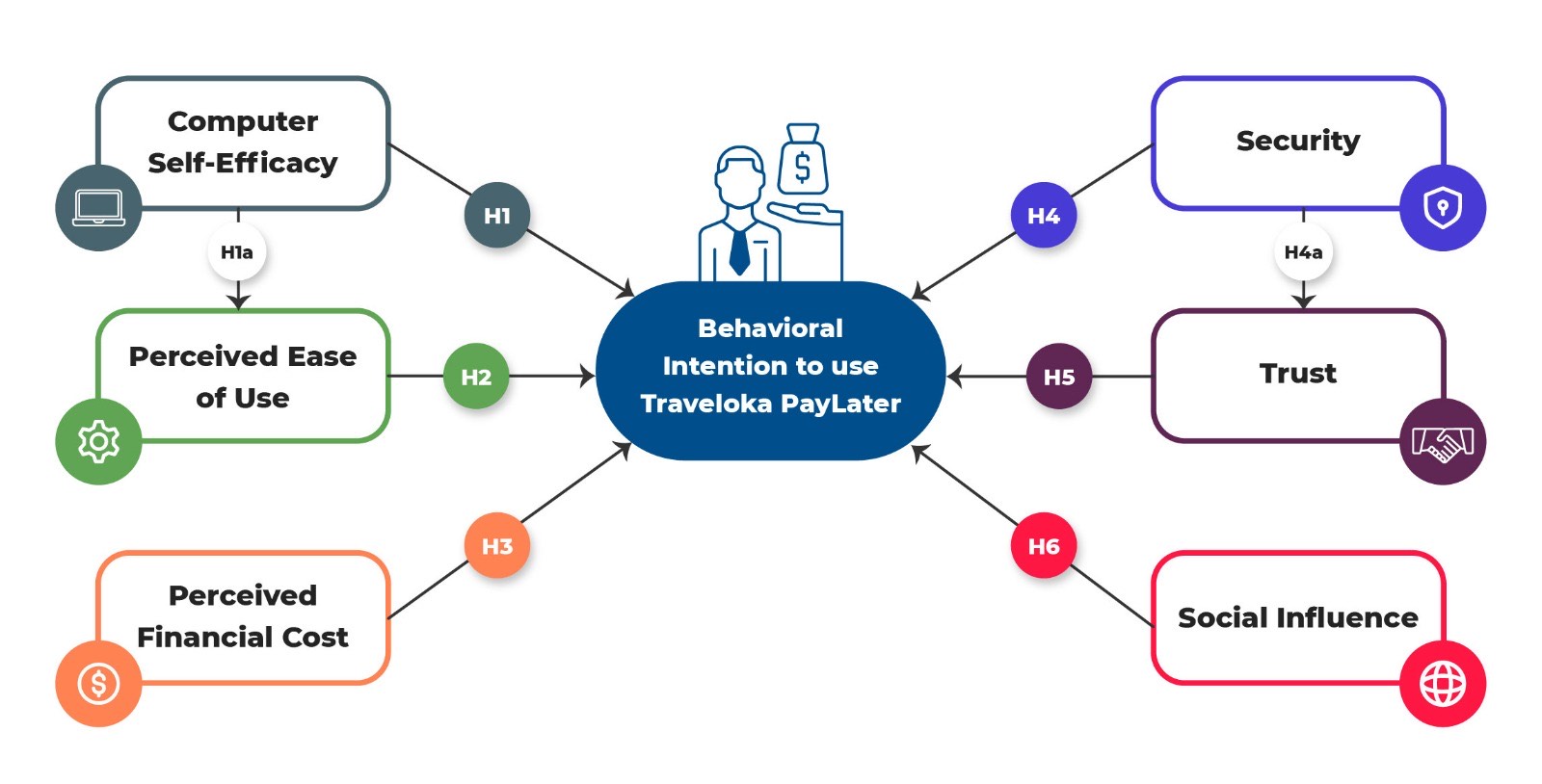

Дослідження показало, що комп'ютерна самоефективність впливає на сприйману простоту використання, безпека здійснює вплив на довіру, а соціальний вплив впливає на поведінковий намір використовувати Traveloka Paylater. Тим часом, комп'ютерна самоефективність, сприймана простота використання, сприймані фінансові витрати, безпека та довіра не мають позитивного впливу на поведінкові наміри використовувати Traveloka Paylater.

Користувачам з більш високим рівнем комп'ютерної самоефективності простіше користуватися сервісами і вони більше довіряють платформі з більш високим рівнем безпеки. Доведено, що соціальні мережі мають найбільший вплив на потенційних користувачів, заохочуючи їх користуватися послугами Traveloka Paylater. Оскільки сервіси Traveloka Paylater також пропонують привабливі акції, включаючи знижки, користувачі не заперечуватимуть проти додаткових витрат.

Дослідження показує, що Traveloka Paylater стає привабливим сервісом цифрових платежів завдяки своєму взаємозв'язку з механізмом кредитної системи, який дозволяє покупцям здійснювати покупки зараз, а платити пізніше в розстрочку. Traveloka Paylater демонструє перспективу зростання, оскільки індонезійці вже знайомі з кредитною системою. Оскільки більшість користувачів Traveloka Paylater складають молоде покоління, такий спосіб оплати приносить задоволення від імпульсивних покупок.

Для збільшення кількості цільових користувачів старшого покоління, дослідження виявило необхідність надання більш інтегрованих простих методів реєстрації, а також створення привабливих функцій живого чату, регулярного моніторингу системи та роботи з відомими впливовими особами для підвищення грамотності.

Спонсор дослідження

- The authors gratefully acknowledge to Universitas Multimedia Nusantara, Indonesia that provided support for this research.

Посилання

- Asosiasi Penyelenggara Jasa Internet Indonesia. Laporan Survei Internet APJII and Indonesia Survey Center 2019–2022 (Q2).

- Kurniasari, F., Riyadi, W. T. (2021). Determinants of Indonesian E-Grocery Shopping Behavior After Covid-19 Pandemic Using the Technology Acceptance Model Approach. United International Journal for Research & Technology (UIJRT), 3 (1), 12–18. Available at: https://uijrt.com/articles/v3/i1/UIJRTV3I10003.pdf

- Layanan Paylater untuk Liburan, Jalan-jalan Dulu Bayar Kemudian (2022). Kompas. Available at: https://travel.kompas.com/read/2022/07/22/181742427/4-layanan-paylater-untuk-liburan-jalan-jalan-dulu-bayar-kemudian?page=all

- Shofa, J. N. (2020). Ini Perbedaan Layanan Paylater dan Kartu Kredit. Available at: https://www.beritasatu.com/digital-life/665965/ini-perbedaan-layanan-paylater-dan-kartu-kredit

- Gharaibeh, M. K., Arshad, M. R., Gharaibeh, N. K. (2018). Using the UTAUT2 Model to Determine Factors Affecting Adoption of Mobile Banking Services: A Qualitative Approach. International Journal of Interactive Mobile Technologies (iJIM), 12 (4), 123–134. doi: https://doi.org/10.3991/ijim.v12i4.8525

- Duke, P., Andy, M., Andrew, C. (2019). Insights into Payments Payment Methods Report 2019 Innovations in the Way We Pay. The Paypers, 144, 1–143.

- Arslan, B. (2015). The influence of credit card usage on impulsive buying. International Journal of Physical and Social Sciences, 5 (7), 235–251.

- Chauhan, M., Shingari, I. (2017). Future of e-Wallets: A Perspective From Under Graduates’. International Journal of Advanced Research in Computer Science and Software Engineering, 7 (8), 146. doi: https://doi.org/10.23956/ijarcsse.v7i8.42

- Kurniasari, F., Gunardi, A., Putri, F. P., Firmansyah, A. (2021). The role of financial technology to increase financial inclusion in Indonesia. International Journal of Data and Network Science, 5, 391–400. doi: https://doi.org/10.5267/j.ijdns.2021.5.004

- Alalwan, A. A., Dwivedi, Y. K., Rana, N. P. (2017). Factors influencing adoption of mobile banking by Jordanian bank customers: Extending UTAUT2 with trust. International Journal of Information Management, 37 (3), 99–110. doi: https://doi.org/10.1016/j.ijinfomgt.2017.01.002

- Gulati, S., Nadeau, M.-C., Rajgopal, K. (2015). McKinsey on Payments. McKinsey&Company, 8 (21). Available at: https://www.mckinsey.com/~/media/mckinsey/industries/financial%20services/our%20insights/gauging%20the%20disruptive%20potential%20of%20digital%20wallets/gauging%20the%20disruptive%20potential%20of%20digital%20wallets.ashx

- Macedo, I. M. (2017). Predicting the acceptance and use of information and communication technology by older adults: An empirical examination of the revised UTAUT2. Computers in Human Behavior, 75, 935–948. doi: https://doi.org/10.1016/j.chb.2017.06.013

- Nurcahyani, I. (2022). Transformasi Traveloka Dalam Satu Dekade. Antaranews. Available at: https://www.antaranews.com/berita/2756569/transformasi-traveloka-dalam-satu-dekade?#:~:text=Hingga%20saat%20ini%2C%20aplikasi%20Traveloka,populer%20di%20kawasan%20Asia%20Tenggara

- Choshaly, S. H., Tih, S. (2017). The factors associated with the behavioural intention of ecolabelled products. Journal of Social Sciences & Humanities, 25, 196–206.

- Adams, P., Farrell, M., Dalgarno, B., Oczkowski, E. (2017). Household Adoption of Technology: The Case of High-Speed Broadband Adoption in Australia. Technology in Society, 49, 37–47. doi: https://doi.org/10.1016/j.techsoc.2017.03.001

- E-commerce Payments Trends: Indonesia’s e-commerce market trends: Major growth boosted by economic gains (2023). J.P. Morgan Global Payment Trends.

- Kemppainen, K. (2017). Digitalisation: Shaping the retail payment markets while posing new challenges to authorities. Journal of Payments Strategy & Systems, 11 (1), 42–47.

- Ng, D. (2018). Evolution of digital payments: Early learnings from Singapore’s cash-less payment drive. Journal of Payments Strategy & Systems, 11 (4), 306–312.

- Bandura, A. (1977). Self-efficacy: Toward a unifying theory of behavioral change. Psychological Review, 84 (2), 191–215. doi: https://doi.org/10.1037/0033-295x.84.2.191

- Prabhakaran, S., Vasantha, S. (2020). Effect of Social Influence on Intention to Use Mobile Wallet with the Mediating Effect of Promotional Benefits. Journal of Xi’an University of Architecture & Technology, XII (II), 3003–3019.

- Palm, M. (2017). Then press enter: digital payment technology and the history of telephone interface. Cultural Studies, 32 (4), 582–599. doi: https://doi.org/10.1080/09502386.2017.1384034

- Gangwani, R., Cain, A., Collins, A., Cassidy, J. M. (2022). Leveraging Factors of Self-Efficacy and Motivation to Optimize Stroke Recovery. Frontiers in Neurology, 13. doi: https://doi.org/10.3389/fneur.2022.823202

- Ariff, M. S. M., Yeow, S. M., Zakuan, N., Jusoh, A., Bahari, A. Z. (2012). The Effects of Computer Self-Efficacy and Technology Acceptance Model on Behavioral Intention in Internet Banking Systems. Procedia - Social and Behavioral Sciences, 57, 448–452. doi: https://doi.org/10.1016/j.sbspro.2012.09.1210

- Review of buy now pay later arrangements (2018). ASIC.

- McGowan, M. (2017). Afterpay: buy-now pay-later scheme soars in popularity but experts sound warning. Available at: https://www.theguardian.com/australia-news/2017/sep/21/afterpay-buy-now-pay-later-scheme-soars-in-popularity-but-experts-sound-warning

- Mitchell, S., Qadar, S. (2019). Afterpay, PayPal and Zip Pay: The shopping tech making us buy more. Available at:: https://www.abc.net.au/everyday/afterpay-paypal-and-zip-pay-making-us-buy-more/11604216

- Chatterjee, P., Rose, R. L. (2012). Do Payment Mechanisms Change the Way Consumers Perceive Products? Journal of Consumer Research, 38 (6), 1129–1139. doi: https://doi.org/10.1086/661730

- Damghanian, H., Zarei, A., Siahsarani Kojuri, M. A. (2016). Impact of Perceived Security on Trust, Perceived Risk, and Acceptance of Online Banking in Iran. Journal of Internet Commerce, 15 (3), 214–238. doi: https://doi.org/10.1080/15332861.2016.1191052

- Soman, D. (2001). Effects of Payment Mechanism on Spending Behavior: The Role of Rehearsal and Immediacy of Payments. Journal of Consumer Research, 27 (4), 460–474. doi: https://doi.org/10.1086/319621

- Kurniasari, F., Abd Hamid, N., Qinghui, C. (2020). The effect of perceived usefulness, perceived ease of use, trust, attitude and satisfaction into continuance intention in using alipay. Management & Accounting Review, 19 (2).

- Prastiwi, I. E., Fitria, T. N. (2021). Konsep Paylater Online Shopping dalam Pandangan Ekonomi Islam. Jurnal Ilmiah Ekonomi Islam, 7 (1), 425. doi: https://doi.org/10.29040/jiei.v7i1.1458

- Abdullah, F., Ward, R., Ahmed, E. (2016). Investigating the influence of the most commonly used external variables of TAM on students’ Perceived Ease of Use (PEOU) and Perceived Usefulness (PU) of e-portfolios. Computers in Human Behavior, 63, 75–90. doi: https://doi.org/10.1016/j.chb.2016.05.014

- Mwiya, B., Chikumbi, F., Shikaputo, C., Kabala, E., Kaulung’ombe, B., Siachinji, B. (2017). Examining Factors Influencing E-Banking Adoption: Evidence from Bank Customers in Zambia. American Journal of Industrial and Business Management, 07 (06), 741–759. doi: https://doi.org/10.4236/ajibm.2017.76053

- Saprikis, V., Avlogiaris, G., Katarachia, A. (2022). A Comparative Study of Users versus Non-Users’ Behavioral Intention towards M-Banking Apps’ Adoption. Information, 13 (1), 30. doi: https://doi.org/10.3390/info13010030

- Chua, E. L., Chiu, J. L., Chiu, C. L. (2020). Factors influencing trust and behavioral intention to use Airbnb service innovation in three ASEAN countries. Asia Pacific Journal of Innovation and Entrepreneurship, 14 (2), 175–188. doi: https://doi.org/10.1108/apjie-12-2019-0095

- Riffai, M. M. M. A., Grant, K., Edgar, D. (2012). Big TAM in Oman: Exploring the promise of on-line banking, its adoption by customers and the challenges of banking in Oman. International Journal of Information Management, 32 (3), 239–250. doi: https://doi.org/10.1016/j.ijinfomgt.2011.11.007

- Agrawal, A. (2018). The Effects of Immediate and Delayed Payments on Consumption Behavior. ETD collection for University of Nebraska - Lincoln. Available at: https://digitalcommons.unl.edu/dissertations/AAI10837673/

- Singh, S., Srivastava, R. K. (2018). Predicting the intention to use mobile banking in India. International Journal of Bank Marketing, 36 (2), 357–378. doi: https://doi.org/10.1108/ijbm-12-2016-0186

- Folkinshteyn, D., Lennon, M. (2016). Braving Bitcoin: A technology acceptance model (TAM) analysis. Journal of Information Technology Case and Application Research, 18 (4), 220–249. doi: https://doi.org/10.1080/15228053.2016.1275242

- Vejačka, M., Štofa, T. (2017). Influence of security and trust on electronic banking adoption in Slovakia. E+M Ekonomie a Management, 20 (4), 135–150. doi: https://doi.org/10.15240/tul/001/2017-4-010

- Cheng, F. M., Phou, S., Phuong, S. (2018). Factors Influencing on Consumer’s Digital Payment Adaptation – A Comparison of Technology Acceptance Model and Brand Knowledge. Proceedings of the 21st Asia-Pacific Conference on Global Business, Economics, Finance & Social Sciences (AP18Taiwan Conference). Taipei.

- Yao, M., Di, H., Zheng, X., Xu, X. (2018). Impact of payment technology innovations on the traditional financial industry: A focus on China. Technological Forecasting and Social Change, 135, 199–207. doi: https://doi.org/10.1016/j.techfore.2017.12.023

- Yap, L., Khoo, G. L. (2022). An Investigation to Examine Factors Influencing University Students’ Behavioral Intention Towards the Acceptance of Brightspace LMS: Using SEM Approach. ACE Official Conference Proceedings. doi: https://doi.org/10.22492/issn.2186-5892.2022.24

- Ho, J. C., Wu, C.-G., Lee, C.-S., Pham, T.-T. T. (2020). Factors affecting the behavioral intention to adopt mobile banking: An international comparison. Technology in Society, 63, 101360. doi: https://doi.org/10.1016/j.techsoc.2020.101360

- Garg, N., Garg, N. (2019). Blockchain Revolutionizing Industry 4.0 (Decentralize Technology for Industries Automation). Global Journal of Enterprise Information System, 11 (4), 70–72.

- Fang, S., Xu, L. D., Zhu, Y., Ahati, J., Pei, H., Yan, J., Liu, Z. (2014). An Integrated System for Regional Environmental Monitoring and Management Based on Internet of Things. IEEE Transactions on Industrial Informatics, 10 (2), 1596–1605. doi: https://doi.org/10.1109/tii.2014.2302638

- Yeboah, A., Owusu-Prempeh, V. (2017). Exploring the Consumer Impulse Buying Behaviour from a Range of Consumer and Product Related Factors. International Journal of Marketing Studies, 9 (2), 146. doi: https://doi.org/10.5539/ijms.v9n2p146

- Hair, J. F., Risher, J. J., Sarstedt, M., Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31 (1), 2–24. doi: https://doi.org/10.1108/ebr-11-2018-0203

##submission.downloads##

Опубліковано

Як цитувати

Номер

Розділ

Ліцензія

Авторське право (c) 2023 Florentina Kurniasari, Johny Natu Prihanto, Nikolaus Andre

Ця робота ліцензується відповідно до Creative Commons Attribution 4.0 International License.

Закріплення та умови передачі авторських прав (ідентифікація авторства) здійснюється у Ліцензійному договорі. Зокрема, автори залишають за собою право на авторство свого рукопису та передають журналу право першої публікації цієї роботи на умовах ліцензії Creative Commons CC BY. При цьому вони мають право укладати самостійно додаткові угоди, що стосуються неексклюзивного поширення роботи у тому вигляді, в якому вона була опублікована цим журналом, але за умови збереження посилання на першу публікацію статті в цьому журналі.

Ліцензійний договір – це документ, в якому автор гарантує, що володіє усіма авторськими правами на твір (рукопис, статтю, тощо).

Автори, підписуючи Ліцензійний договір з ПП «ТЕХНОЛОГІЧНИЙ ЦЕНТР», мають усі права на подальше використання свого твору за умови посилання на наше видання, в якому твір опублікований. Відповідно до умов Ліцензійного договору, Видавець ПП «ТЕХНОЛОГІЧНИЙ ЦЕНТР» не забирає ваші авторські права та отримує від авторів дозвіл на використання та розповсюдження публікації через світові наукові ресурси (власні електронні ресурси, наукометричні бази даних, репозитарії, бібліотеки тощо).

За відсутності підписаного Ліцензійного договору або за відсутністю вказаних в цьому договорі ідентифікаторів, що дають змогу ідентифікувати особу автора, редакція не має права працювати з рукописом.

Важливо пам’ятати, що існує і інший тип угоди між авторами та видавцями – коли авторські права передаються від авторів до видавця. В такому разі автори втрачають права власності на свій твір та не можуть його використовувати в будь-який спосіб.